Lowest interest rates for home Loans

If you have too much debt to qualify for a conventional mortgage, less than stellar credit scores or not much cash for a down payment, consider buying a home with an FHA loan.

If you have too much debt to qualify for a conventional mortgage, less than stellar credit scores or not much cash for a down payment, consider buying a home with an FHA loan.

The Federal Housing Administration, a division of the Department of Housing and Urban Development, was created 80 years ago to help low- and moderate-income families borrow the money they need to buy a home.

The FHA doesn't actually make home loans. It guarantees that lenders will be repaid if you default on the loan.

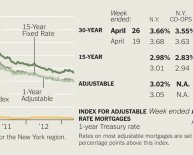

That guarantee allows banks and mortgage companies to work with borrowers who might not be able to qualify for conventional home loans and at surprisingly competitive interest rates.

The majority of lenders make these mortgages, and about 1 in 6 new home loans is backed by the FHA, according to Ellie Mae, a California-based mortgage technology firm.

There are serious limits on how much you can borrow with an FHA loan for a single-family home — up to $271, 050 for single-family homes in most parts of the country or as much as $625, 500 in high-cost cities such as New York and San Francisco.

But if the amount you need falls within those guidelines, here are the advantages to getting an FHA loan.

Advantage 1. You'll need a smaller down payment.

Most FHA mortgages require a 3.5% down payment — that's $3, 500 for every $100, 000 you borrow — and the average down payment on an FHA home loan is about 4%, according to Ellie Mae.

That's far less than the 20% average for conventional home loans.

Your down payment can be a gift from a relative, a friend or an organization that provides financial assistance.

Many conventional mortgages require the down payment to come from a borrower's savings or other assets, such as proceeds from the sale of another home.

Advantage 2. You can qualify with below-average credit.

The average FICO score for buyers who finance FHA loans is 687, according to Ellie Mae.

That's considerably lower than the average score of 754 for conventional, non-FHA financing.

So what's the secret to qualifying if you have a credit score in the low 700s or high 600s?

Successful applicants usually have a two-year history of steady employment and paying their bills on time.

You can get an FHA loan if you're self-employed. Just be ready to document your income with tax returns and financial statements from your business.

The same big financial problems that derailed FHA applications in the past continue to do so. If you:

- Declared Chapter 7 bankruptcy, you usually must wait two years from the date of discharge before qualifying.

- Lost a home through foreclosure, you must wait three years. However, if you can prove that the foreclosure was caused by involuntary job loss or income reduction, and your payment history has been good since then, the waiting period can be as little as one year.

- Are delinquent on a federal debt, such as a student loan or income taxes, you can't get an FHA loan.

- Have a credit score lower than 500, you won't qualify under FHA guidelines. Most lenders have a higher minimum of 600.

Share this article

Related Posts

Latest Posts