Best Fixed rate Mortgage Deals 5 years

Mortgage Rates For ARMs & Fixed Rate Loans

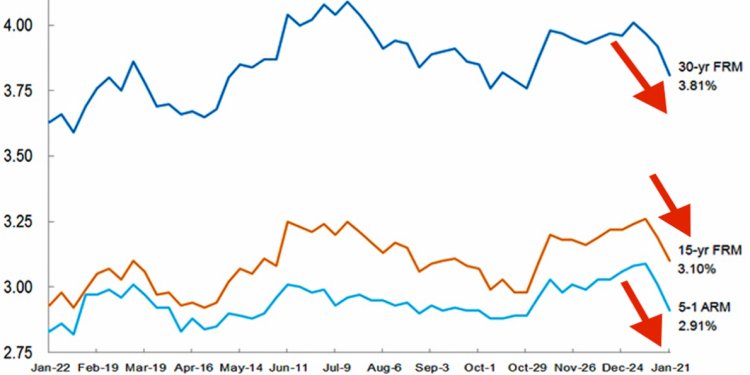

As recently as 10 years, mortgage borrowers had tens of choices with respect to picking "the best mortgage" for their needs. Today, there are basically two - fixed-rate mortgages (FRM) and adjustable-rate mortgages (ARM).

It can be confusing to know which loan type is best for your individual needs; and, lenders ask basic questions to help you decide whether to go with an ARM or fixed.

- How long do you plan to stay in the home?

- Are you comfortable with the idea of "changing mortgage payments?"

There are no right or wrong answers, necessarily, but after understanding the benefits and risks of fixed-rate mortgages and adjustable-rate mortgages, as a home buyer or refinancing household, you'll be in a better position to choose the loans that's right for you.

All About Fixed Rate Mortgages

A fixed-rate mortgage is exactly what it sounds like. It's a mortgage for which the interest rate is fixed for the life of the loan.

Fixed rate mortgages are available in multiple terms, where "term" is used to describe the length for which the mortgage contract is in place. With fixed-rate mortgages, when the term is complete, the loan is paid-in-full.

The monthly payment on a fixed-rate loan is inversely proportional to its term. The more years in a loan, the lower its monthly payment. This is because, with a shorter loan term, the homeowner repays its lender over a lesser period of time.

The most common loan terms are 30 years and 15 years. 20-year terms and 10-year terms are common, too.

The benefits of a shorter-term loan are lower mortgage rates as compared to longer-term loans; and less mortgage interest paid to the lender over time.

- 30-year fixed rate mortgage : $2, 993 monthly; $452, 000 interest over time

- 20-year fixed rate mortgage : $3, 749 monthly; $274, 000 interest over time

- 15-year fixed rate mortgage : $4, 383 monthly; $163, 000 interest over time

- 10-year fixed rate mortgage : $6, 040 monthly; $99, 000 interest over time

Some banks also offer intermediate loan terms including the 25-year fixed rate mortgage and odd-year terms such as a 17-year fixed rate mortgage.

The main benefits of a fixed rate mortgage are linked to its predictability. With a fixed-rate mortgage, your mortgage payment is set on Day 1 of your home loan, and never changes until the loan is paid-in-full. Some homeowners prefer this sort of certainty.

However, in recent years, fixed-rate loans have offered an additional benefit to certain refinancing households.

Homeowners using a fixed-rate loan can have LTVs of 125% or higher. Households using the program's adjustable-rate feature are limited to a loan-to-value of just 105 percent.

All About Adjustable-Rate Mortgages

An adjustable-rate mortgage (ARM) is a mortgage for which the interest rate can vary over time.

Mortgage rates are often lower with an adjustable-rate mortgage versus for a comparable fixed rate loan because the homeowner assumes some of the long-term interest rate risk which is fully-assigned to the bank with a fixed-rate loan.

Most ARMs works like this :

- For some preset, fixed number of years, the ARM's mortgage rate remains unchanged

- After the fixed period ends, the mortgage rate changes based on a preset formula

- Annually, the ARM's mortgage rate changes again based on the same formula

The majority of today's adjustable-rate mortgages adjust once annually until the original loan balance has been paid in full - a process which last as long as the loan's term (e.g.; 30 years, 15 years).

Note that some ARMs exist which adjust every six months, but they are uncommon. Annual adjustments are most prevalent.

When ARMs adjust, the "adjusted mortgage rate" is a sum of two numbers - a constant figure called a margin and a variable figure called an index. When you add the (margin) to the (index), you get your new rate.

Share this article

FAQ

What US banks offer foreign national mortgages? - Quora

Find a local, licensed loan originator who works for a non-depository mortgage lender OR a mortgage broker. Either of these entities (and not a bank) will be able to help you locate a lender willing to lend. You do not have to be a U.S. citizen to obtain a mortgage in the U.S. Here's another trick. The industry uses this website as a way to shop and see what lenders have to offer their customers:

Related Posts

Latest Posts